Emergency Fund How Much Should You Save? | Guide

Most financial advisors recommend saving 3 to 6 months of expenses in an emergency fund, but the reality is far more nuanced. Your ideal emergency fund amount depends on your income stability, household composition, health conditions, job security, and risk tolerance. A single freelance graphic designer in San Francisco has vastly different needs than a tenured teacher in Ohio with two dependents and a spouse’s stable income.

This guide breaks down exactly how much you should save, explains the factors that determine your number, and provides actionable strategies to build your fund—even if you’re starting from zero.

The Short Answer: How Much Do You Actually Need?

Quick Answer: Most Americans need 3 to 6 months of essential living expenses in an emergency fund. Single-income households, freelancers, and those in volatile industries should aim for 6 to 9 months. Dual-income households with stable jobs may function comfortably at 3 months.

📊 KEY STATS

- 69% of Americans have less than $1,000 in savings

- Only 41% of adults could cover a $1,000 emergency with savings

- 58% of bankruptcies are caused by medical emergencies

- The average American household spends $5,111 per month on essentials

- 1 in 3 workers experienced a job loss or reduction in 2023-2024

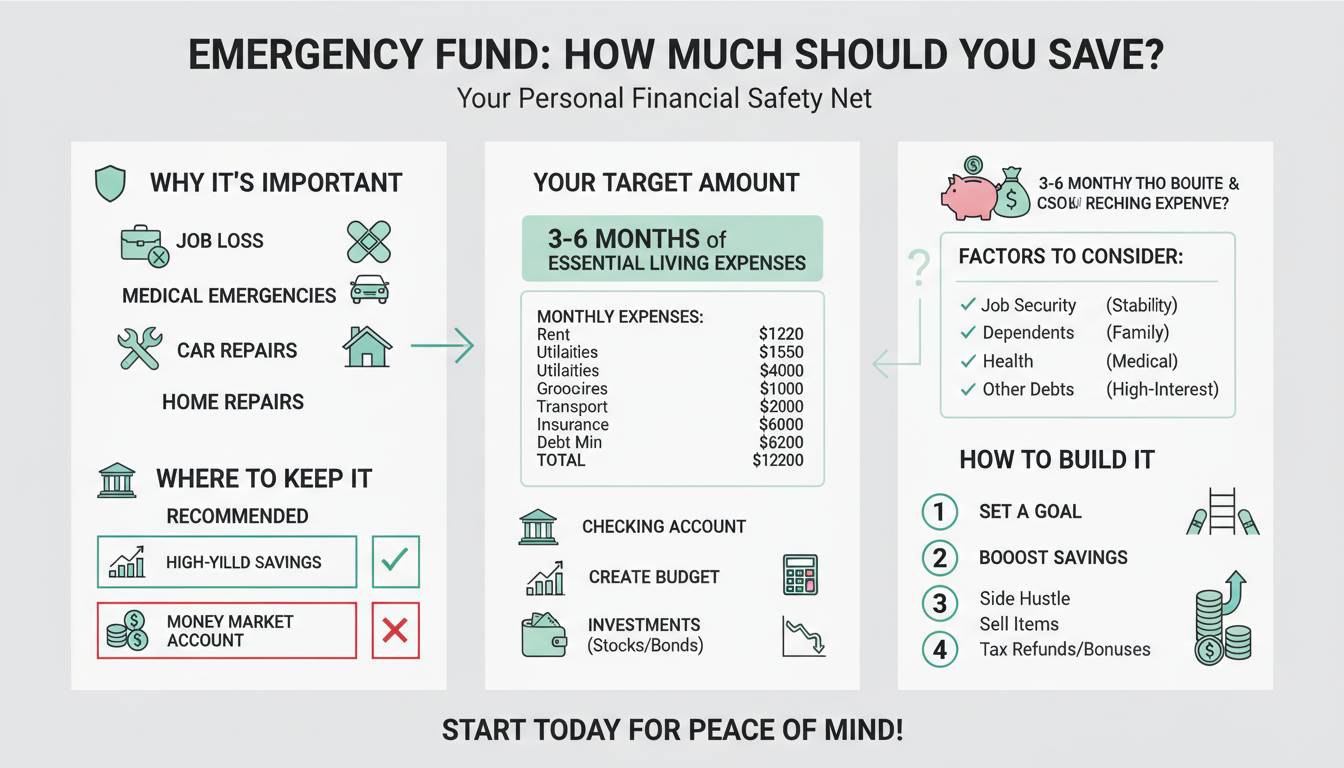

The 3-to-6-month guideline exists because it covers most scenarios: job loss, medical emergencies, major home repairs, or unexpected travel. However, this range represents a starting point, not a one-size-fits-all mandate.

Understanding Your Emergency Fund

An emergency fund is liquid, easily accessible money set aside specifically to cover essential expenses during unforeseen circumstances. Unlike other savings goals—retirement, a vacation, or a new car—emergency funds exist solely as financial insurance against life’s unpredictability.

What qualifies as an emergency?

- Job loss or significant income reduction

- Medical emergencies not fully covered by insurance

- Critical home repairs (failed HVAC, roof damage, plumbing emergencies)

- Essential vehicle repairs

- Family emergencies requiring travel

- Sudden childcare needs

What does NOT qualify:

- Planned medical procedures

- Vacations or planned trips

- Retail sales or “good deals”

- Upgrading lifestyle

- Debt repayment (except in true hardship situations)

The key distinction: an emergency is unexpected, necessary, and urgent. If you can plan for it or choose not to spend money on it, it’s not an emergency.

The 3-to-6-Month Rule Explained

The 3-to-6-month guideline has become personal finance conventional wisdom, but understanding why this range exists helps you determine where you fall within it.

Why 3 months works for some households:

Dual-income households where both partners have stable employment, predictable industries, and strong job markets can often manage with 3 months of reserves. If one partner loses income, the other can typically cover most essentials while the job search continues. These households have lower risk exposure.

Why 6 months is safer for others:

Single-income households, freelancers, gig workers, and those in cyclical industries (construction, retail, hospitality) face higher income volatility. Six months provides a longer runway to find new employment without draining retirement accounts or accumulating high-interest debt.

The case for 9+ months:

Some financial planners recommend 9 to 12 months for:

- Single parents with sole income responsibility

- Self-employed individuals with irregular income

- Those with chronic health conditions requiring ongoing care

- Primary earners in age groups where job re-entry takes longer

- Households in high-cost-of-living areas with limited local job options

Factors That Change Your Ideal Amount

Your emergency fund target isn’t arbitrary—it should reflect your specific financial circumstances. Consider these variables:

Income Stability

| Income Type | Recommended Fund |

|---|---|

| Tenured government employee | 3 months |

| Large corporation, strong performance | 3-4 months |

| Small business employee | 4-6 months |

| Freelance/Commission-based | 6-9 months |

| Self-employed | 6-12 months |

Household Composition

Single individuals without dependents can often operate on the lower end of the range—their expenses are typically lower, and their financial obligations are simpler. Families with children, especially single-parent households, need larger reserves because children’s needs are non-negotiable and alternative care options during a crisis are limited.

Health Considerations

Households with chronic health conditions, disabilities, or family histories suggesting elevated health risks should build larger emergency funds. Even with good insurance, deductibles, co-pays, and out-of-pocket maximums can quickly consume thousands of dollars.

Industry and Job Market

Technology workers in hot job markets can often find new positions within weeks. Workers in niche fields, academic positions, or industries experiencing downturns may face months of unemployment. Geographic factors matter too—areas with lower unemployment rates offer faster re-employment.

Existing Safety Nets

If you have access to other resources—family support, substantial taxable investment accounts, home equity you could access, or a working spouse with stable income—your emergency fund requirement decreases. These represent alternative buffers, even if less convenient than cash.

How to Calculate Your Exact Number

Calculating your target emergency fund requires accurate numbers, not estimates. Here’s the step-by-step process:

Step 1: Identify Essential Expenses

Calculate your monthly “bare bones” budget—the minimum you need to survive comfortably without cutting deeply into health, safety, or basic functioning.

| Category | Monthly Amount |

|---|---|

| Housing (rent/mortgage) | $ |

| Utilities (electric, gas, water, internet) | $ |

| Groceries | $ |

| Transportation (car payment, gas, insurance) | $ |

| Minimum debt payments | $ |

| Insurance (health, car, life if applicable) | $ |

| Childcare/Essential subscriptions | $ |

| Medications/Medical supplies | $ |

| TOTAL | $ |

Step 2: Multiply by Your Target Months

Once you have your monthly essential total, multiply by 3, 6, or 9 depending on your risk profile:

- 3 months: Stable dual-income, employed in growing industries

- 4-5 months: Moderate risk factors present

- 6 months: Standard recommendation for most Americans

- 7-9 months: Higher risk profiles (self-employed, single income)

- 9-12 months: Maximum security for highest-risk situations

Step 3: Add Category-Specific Buffers

Consider adding specific buffers for:

- Health insurance deductible: Add $1,000-$5,000 depending on your plan

- Car repair fund: Add $1,000-$2,000 for vehicle emergencies

- Home maintenance: Add $2,000-$5,000 if you’re a homeowner

- Professional development: Add $500-$1,000 for certifications or training if job hunting requires skill upgrades

Building Your Fund: A Month-by-Month Approach

Reaching your target takes time, but systematic saving accelerates the process. Here’s how to build strategically:

Phase 1: Seed Your Fund ($1,000-$2,000)

Before aggressive saving, establish a small baseline. This covers minor emergencies—car repairs, small medical bills, appliance failures—without derailing your budget.

Action: Save $500-$1,000 as quickly as possible, even if it requires temporary side work or reducing discretionary spending.

Phase 2: Expand to One Month

Build toward covering one month of essential expenses. This milestone provides meaningful protection while you continue building.

Timeline: Most households reach this within 2-4 months with focused effort.

Phase 3: Reach Three Months

Three months represents the minimum safety net for most situations. Celebrate this milestone—you now have meaningful protection against unexpected events.

Phase 4: Push to Six Months

Continue contributions until reaching your target based on risk profile. Automate transfers on payday to remove decision fatigue.

Strategies That Accelerate Growth

Direct deposit split: Have your paycheck split between checking and savings automatically.

Windfall allocation: Direct 50-100% of tax refunds, bonuses, side hustle income, and gifts to your emergency fund until fully funded.

Expense challenges: Try no-spend weeks, cancel unused subscriptions, or challenge yourself to reduce one category for 90 days and redirect those savings.

Side income: Consider a consistent side gig—even $200/month adds $2,400 annually and significantly accelerates your timeline.

Where to Keep Your Emergency Money

Your emergency fund serves no purpose if you can’t access it quickly. Location matters as much as contribution habits.

High-Yield Savings Accounts (Recommended Primary)

| Account Type | Typical APY | Access Time | FDIC Insured |

|---|---|---|---|

| Online High-Yield Savings | 4.25%-4.75% | 1-2 business days | Yes |

| Traditional Savings | 0.01%-0.05% | Same day | Yes |

| Money Market Accounts | 4.00%-4.50% | 1-3 business days | Yes |

Online high-yield savings accounts currently offer 10-100 times the interest of traditional banks. The difference amounts to hundreds of dollars annually on balances of $10,000 or more—with zero added risk since FDIC insurance covers both.

Recommended accounts (as of 2024):

- Ally Bank (4.20% APY)

- Marcus by Goldman Sachs (4.40% APY)

- Discover Online Savings (4.30% APY)

- Capital One 360 Performance (4.30% APY)

Money Market Funds (Alternative)

Ultra-short-term bond funds (not FDIC insured, but low risk) offer slightly higher yields than savings accounts but carry minimal risk of value fluctuation. These work for funds exceeding FDIC limits, though most emergency funds fall well below coverage thresholds.

What to Avoid

- Certificates of Deposit (CDs): Early withdrawal penalties defeat emergency access

- Investments (stocks, bonds, crypto): Value fluctuation defeats the stability purpose

- Physical cash: Loses value to inflation and isn’t secure

- Retirement accounts: Penalties and taxes make this expensive emergency access

When to Adjust Your Target

Your emergency fund isn’t a “set and forget” number. Life changes necessitate recalibration:

Increase Your Target When:

- Starting self-employment or freelancing

- Becoming a single-income household

- Having a child or becoming a single parent

- Experiencing a health diagnosis (yours or family member)

- Entering a volatile industry or company

- Relocating to a high-cost area

Decrease Your Target When:

- Securing stable, long-term employment

- Paying off debt that represented significant risk

- Building alternative safety nets (investable assets, spouse’s stable income)

- Reaching retirement with diversified income sources (Social Security, pensions, withdrawals)

Annual Review Recommendation

Review your emergency fund target annually—typically around tax season or your birthday—when you’re already thinking about financial planning. Adjust based on life changes and recalculate your target number.

Common Emergency Fund Mistakes

Avoid these frequently observed errors:

Mistake #1: Never Starting Because Target Seems Unreachable

Saving $20,000 feels impossible when you have nothing. Saving $500 is achievable. Start with the smallest milestone—$1,000—rather than paralyzed by the full target.

Solution: Break your goal into micro-targets. Celebrate each milestone independently.

Mistake #2: Keeping Fund in Checking Account

Money in checking earns nothing and gets spent accidentally. Keep emergency funds separate—out of sight, out of mind, but accessible.

Mistake #3: Using Emergency Fund for Non-Emergencies

Every “great deal” or “once-in-a-lifetime opportunity” isn’t an emergency. Dipping into your fund for discretionary expenses defeats its purpose.

Solution: Establish a clear definition of “emergency” and commit to it. If you struggle, keep cash in a less accessible account.

Mistake #4: Over-Funding at Expense of Other Goals

While emergency funds are crucial, hoarding excessive cash while carrying high-interest debt or missing employer 401(k) matches costs money. Balance is key.

Guideline: If you have high-interest debt (credit cards, personal loans), consider a moderate emergency fund ($2,000-$3,000) while attacking debt, then fully fund afterward.

Frequently Asked Questions

How long does it take to build a 6-month emergency fund?

The timeline depends on your income and expenses. Saving 10% of income toward your fund, the average household takes 2-4 years to reach 6 months. Aggressive saving (20-30% of income) can achieve this in 12-18 months. Using windfalls like tax refunds accelerates the timeline significantly.

Should I include investments in my emergency fund?

No. Emergency funds should be kept in cash or cash equivalents (high-yield savings, money market accounts). Investment values fluctuate, which defeats the stability purpose. The slight return potential isn’t worth the risk of your emergency money being worth less when you need it.

What if I can’t save 3 months of expenses?

Start smaller. Even $500-$1,000 prevents most emergencies from becoming debt. Focus on building $2,000 first—that covers 70% of typical emergencies. As income increases or expenses decrease, accelerate contributions.

Does my emergency fund need to be in addition to other savings?

Yes. Emergency funds are separate from retirement accounts, vacation savings, vehicle funds, or sinking funds for planned expenses. Once your emergency fund is fully funded, you can allocate savings toward other goals.

Is cash or checking account better for emergency funds?

High-yield savings accounts are significantly better. Traditional checking accounts earn minimal interest (often under 0.05% APY), while online high-yield savings accounts currently offer 4.25-4.75% APY. On a $15,000 emergency fund, this difference is approximately $600-$700 annually.

Should my spouse and I have separate emergency funds?

Most financial experts recommend a joint emergency fund for households, as either partner may face job loss or emergency. However, maintaining a small separate fund ($500-$1,000) for personal emergencies can provide autonomy while the household fund handles major events.

Conclusion: Your Next Steps

The question “how much should I save in my emergency fund?” has no universal answer—but you now have a framework to calculate your specific target. Here’s your action plan:

-

Calculate your number today: Add up essential monthly expenses and multiply by your recommended months (3-6 typically, higher if self-employed or single-income).

-

Open a high-yield savings account: If you don’t have one, online banks offer 10x the interest of traditional banks with FDIC protection.

-

Start with $1,000: Don’t wait for the full target. Get $1,000 saved immediately—that’s your first milestone.

-

Automate contributions: Set up automatic transfers on payday. Treat your emergency fund like a bill you pay yourself.

-

Review annually: Life changes—marriage, children, job changes, health events—should trigger a recalculation of your target.

Your emergency fund is the foundation of financial security. It prevents emergencies from becoming disasters, provides peace of mind, and gives you options when life inevitably changes. Start today, even small, and build systematically toward your target number.