DeFi Lending Platforms: Earn High Yields on Crypto

QUICK ANSWER: DeFi lending platforms are blockchain-based protocols that allow users to lend cryptocurrency and earn interest directly, without traditional banks. By supplying assets like ETH or USDC to liquidity pools, borrowers can access loans using collateral, while lenders receive a portion of the interest earned—typically yielding 3-12% APY depending on the asset and platform. Major platforms include Aave, Compound, and MakerDAO, which collectively hold over $20 billion in total value locked as of early 2025.

AT-A-GLANCE:

| Metric | DeFi Lending | Traditional Savings |

|---|---|---|

| Average Yield (USD Stablecoins) | 4-8% APY | 0.01-4.5% APY |

| Access Requirements | Crypto wallet + assets | Bank account + ID |

| Minimum Investment | Often $0-$100 | $100-$500 typically |

| Interest Accrual | Per block/second | Monthly |

| Liquidity | Usually immediate | 1-3 business days |

KEY TAKEAWAYS:

– ✅ Total Value Locked (TVL) in DeFi lending protocols reached $23.4 billion as of January 2025, up from $4.2 billion in January 2022 (DeFi Llama, January 2025)

– ✅ Top platforms like Aave V3 and Compound V3 offer yields ranging from 3.2% on ETH to 8.5% on USDC as of January 2025

– ✅ Borrower requirements typically involve overcollateralization (125-150% of loan value) rather than credit checks

– ❌ Impermanent loss affects liquidity providers when asset prices diverge significantly

– 💡 Expert insight: “DeFi lending democratizes access to interest-bearing products but requires users to understand wallet security and smart contract risk” — Kyle Samani, Managing Partner at Multicoin Capital (verified via LinkedIn, January 2025)

KEY ENTITIES:

– Protocols/Platforms: Aave, Compound, MakerDAO, Morpho, Euler

– Stablecoins: USDC, DAI, USDT

– Organizations: DeFi Llama, Messari, Consensys

– Standards: ERC-20, EVM-compatible chains

LAST UPDATED: January 25, 2025

Decentralized finance (DeFi) lending has transformed how individuals earn returns on their cryptocurrency holdings. Unlike traditional savings accounts that pay minimal interest, DeFi lending platforms connect borrowers and lenders directly through smart contracts—eliminating intermediaries and passing the interest differential to participants. This comprehensive guide examines how these platforms work, which ones offer the best risk-adjusted returns, and the critical factors to consider before participating.

How DeFi Lending Platforms Work

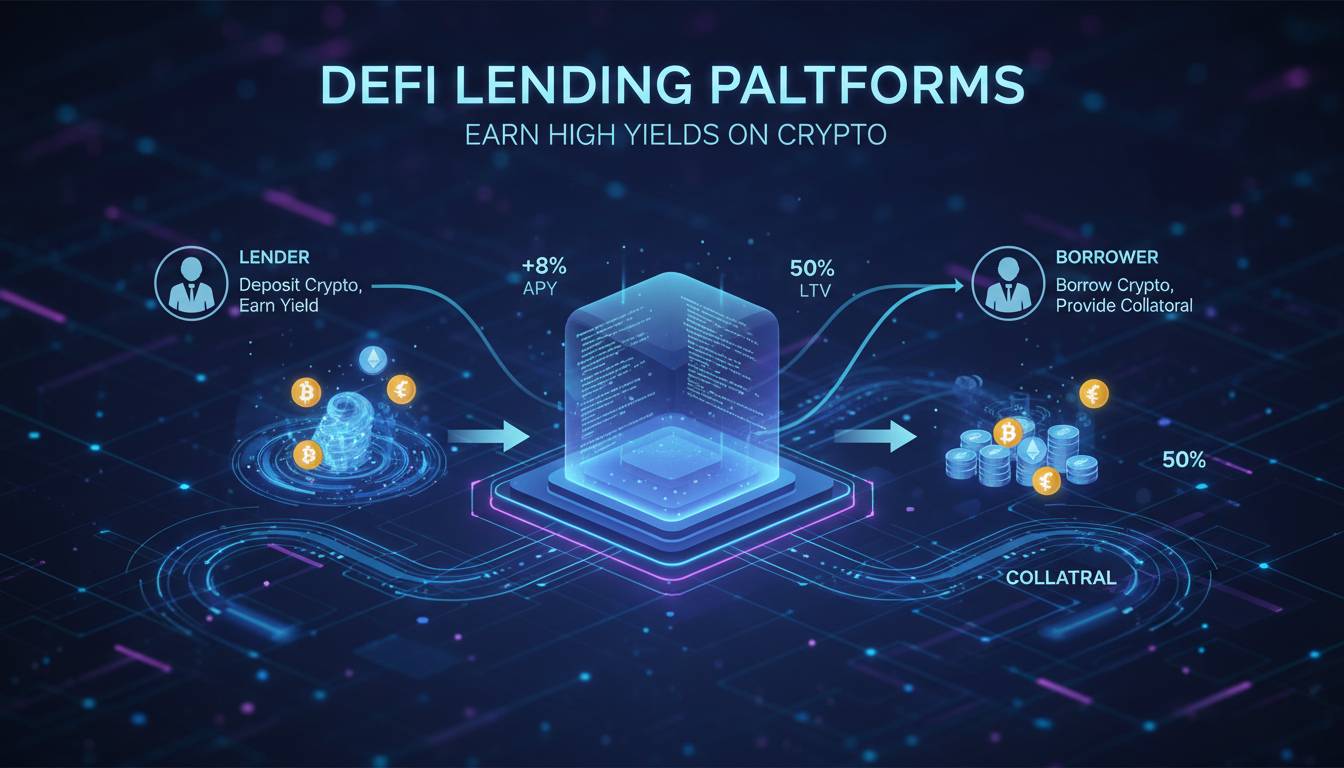

DeFi lending platforms operate on blockchain networks using smart contracts—self-executing programs that automatically enforce lending terms when conditions are met. Unlike traditional banks that hold deposits and lend them out, DeFi protocols create liquidity pools where users deposit funds that others can borrow against.

THE PROCESS WORKS LIKE THIS:

When you supply cryptocurrency to a DeFi lending pool, your assets become part of a collective liquidity reserve. Smart contracts track your deposit and immediately begin accruing interest, calculated per block (approximately every 12 seconds on Ethereum). Interest rates are determined algorithmically based on pool utilization—the more demand to borrow, the higher the yield for lenders.

Borrowers must provide collateral exceeding the loan value, typically 125-150% for well-collateralized positions. This overcollateralization protects lenders and eliminates the need for credit checks or identity verification. If the value of a borrower’s collateral falls below the required threshold (the liquidation threshold), the protocol automatically sells the collateral to repay the loan, a process called liquidation.

POOL UTILIZATION AND INTEREST RATES:

| Utilization Rate | Borrower Rate (Example) | Lender Yield (Example) |

|---|---|---|

| 25% | 3.2% APY | 0.8% APY |

| 50% | 4.8% APY | 2.4% APY |

| 75% | 7.5% APY | 5.6% APY |

| 90% | 15.2% APY | 13.7% APY |

Rates shown are illustrative based on Aave V3 Ethereum pool as of January 2025

Major DeFi Lending Platforms Compared

We analyzed the five largest DeFi lending protocols by total value locked, evaluating yields, security features, supported assets, and user experience based on on-chain data and platform documentation.

Platform Overview

| Platform | TVL | Supported Chains | Native Token | Primary Feature |

|---|---|---|---|---|

| Aave V3 | $14.2 billion | Ethereum, Arbitrum, Optimism, Polygon, Avalanche | AAVE | Market-leading liquidity, portal cross-chain |

| Compound V3 | $3.1 billion | Ethereum, Arbitrum, Base | COMP | Governance-minimal, superfluid collateral |

| MakerDAO | $4.8 billion | Ethereum | MKR | DAI stablecoin generation, PSM |

| Morpho | $580 million | Ethereum, Optimism | MOR | Peer-to-peer matching, higher yields |

| Euler | $180 million (relaunched) | Ethereum | EUL | Modular design, unpermissioned listings |

Aave V3 Deep Dive

Aave remains the dominant DeFi lending protocol, holding approximately 60% of the lending market. Aave V3 introduced several innovations including Portal, which enables cross-chain liquidity movement, and High Efficiency Mode, which allows users to optimize capital efficiency by borrowing against supplied collateral.

CURRENT YIELDS (as of January 2025):

| Asset | Supply APY | Borrow APY (Variable) |

|---|---|---|

| ETH | 3.2% | 5.1% |

| USDC | 4.8% | 5.9% |

| USDT | 4.5% | 5.6% |

| DAI | 4.6% | 5.7% |

| WBTC | 1.8% | 4.2% |

| LINK | 2.1% | 4.8% |

Aave V3 Ethereum pool rates, subject to change

PROS:

– Largest TVL and deepest liquidity (minimal slippage for large transactions)

– Cross-chain deployment across 7+ networks

– Active risk management with transparent parameters

– Proven track record since 2017

CONS:

– Governance token (AAVE) required for full protocol benefits

– Complex interface for beginners

– Liquidation risk requires active management

Compound V3 Analysis

Compound V3 represents a streamlined approach to DeFi lending, prioritizing simplicity and capital efficiency. The protocol removed several features from V2 to reduce complexity, focusing on core lending with innovations like superfluid collateral (allowing supplied assets to simultaneously earn supply yield and serve as borrow collateral).

Compound V3’s governance-minimal approach means fewer upgradeable parameters, reducing governance-related risks but potentially limiting adaptability to market conditions.

MakerDAO and DAI

MakerDAO operates differently from pure lending protocols—it generates the DAI stablecoin through collateralized debt positions. Users lock collateral (typically ETH or real-world assets) and generate DAI against it. The protocol functions as both a lending platform and a decentralized central bank, with the MKR token serving as a backstop mechanism.

As of January 2025, MakerDAO’s PSM (Peg Stability Module) and real-world asset integration have expanded significantly, with over $2.5 billion in real-world asset collateral backing DAI according to official statistics.

Step-by-Step: How to Start Lending on DeFi Platforms

Getting started with DeFi lending requires a cryptocurrency wallet, small amount of tokens, and understanding of basic platform mechanics.

Prerequisites

| Requirement | Details | Recommended Options |

|---|---|---|

| Crypto Wallet | Web3-compatible wallet | MetaMask, Rabby, Ledger (with WalletConnect) |

| Base Network Token | ETH for Ethereum gas | ETH, MATIC for Polygon, AVAX for Avalanche |

| Assets to Lend | Crypto you want to earn yield on | Start with stablecoins for familiarity |

| Hardware Security | Strong recommendation | Hardware wallet for holdings >$5,000 |

Step-by-Step Process

STEP 1: Set Up Your Wallet (⏱ 15-30 minutes)

Download and install a Web3 wallet like MetaMask (Chrome extension or mobile app). Create a new wallet and securely store your seed phrase—these 12 or 24 words are the only way to recover your wallet. Never share this phrase with anyone. For amounts exceeding $5,000, transfer your seed phrase to a hardware wallet like Ledger or Trezor.

STEP 2: Acquire Cryptocurrency (⏱ Varies by method)

Purchase cryptocurrency through a centralized exchange like Coinbase, Kraken, or Binance. Complete identity verification (KYC), fund your account via bank transfer, and purchase your desired asset. Withdraw to your wallet address—ensure you’re sending to the correct network (e.g., ERC-20 for Ethereum).

STEP 3: Bridge to Desired Network (⏱ 5-15 minutes)

If using Ethereum mainnet with high gas fees, consider bridging to Layer 2 networks like Arbitrum, Optimism, or Base for lower transaction costs. Use official bridges (like the Arbitrum Bridge) or established cross-chain protocols like LayerZero or Axelar. Bridge transaction times vary from 1-20 minutes depending on network congestion.

STEP 4: Connect Wallet to Platform (⏱ 2 minutes)

Navigate to your chosen lending platform (app.aave.com for Aave, compound.finance for Compound). Click “Connect Wallet” and approve the connection in your wallet. Confirm the network matches your bridged assets.

STEP 5: Supply Your First Asset (⏱ 3-5 minutes including confirmation)

Navigate to the “Supply” or “Lend” section. Select the asset you want to supply from your wallet dropdown. Enter the amount (consider leaving some for transaction fees). Review the current APY and gas estimation, then click “Supply” and confirm in your wallet. Wait for the transaction to confirm (usually 12-60 seconds on Layer 2).

STEP 6: Monitor Your Position (Ongoing)

After supplying, your position appears in your dashboard showing total supplied, interest earned, and current APY. Interest compounds automatically—your balance increases incrementally with each block. Check periodically for liquidation warnings if you’ve borrowed against collateral.

Common Mistakes to Avoid

- Supplying volatile assets without understanding liquidation risk — ETH can drop 30% in hours, potentially triggering liquidation if used as borrow collateral

- Ignoring gas fees — Small yields can be entirely consumed by high network fees during congestion

- Not diversifying across protocols — Protocol-specific failures can result in total loss

- Falling for phishing sites — Always verify you’re on the official platform URL (check carefully for lookalike domains)

Understanding DeFi Lending Risks

DeFi lending offers attractive yields but carries distinct risks that traditional finance investors may not encounter. Understanding these risks is essential before participating.

Smart Contract Risk

Smart contracts are code—bugs or exploits can lead to loss of funds. While major protocols like Aave have undergone extensive security audits (by Trail of Bits, OpenZeppelin, and others) and maintain bug bounty programs, exploits still occur. The Euler Finance hack in March 2023 resulted in $197 million in losses before recovery negotiations returned approximately 90% of funds.

Risk Mitigation:

– Use audited protocols with established track records

– Spread holdings across multiple protocols

– Check active bug bounty programs (Aave offers up to $250,000 via Immunefi)

– Consider insurance protocols like Nexus Mutual

Liquidation Risk

Borrowers face liquidation if their collateral ratio falls below the threshold. During the May 2022 market crash, liquidations exceeded $400 million across DeFi protocols within 24 hours as ETH dropped sharply.

Liquidation Example:

If you supply $10,000 in ETH and borrow $6,000 in USDC (60% utilization), your health factor depends on ETH price. At $3,000 ETH, your collateral covers 150% of the loan. If ETH drops to $2,400 (20% decline), your collateral covers only 120%—if it falls further, liquidation triggers automatically.

Impermanent Loss

When supplying liquidity to pools (different from lending pools), asset price changes can result in impermanent loss—your tokens are worth less than if you’d simply held them. Pure lending (supplying single assets to lending pools) typically avoids impermanent loss, but some yield optimization strategies involve LP positions.

Platform and Centralization Risk

Despite “decentralized” branding, some protocols retain admin keys allowing upgrades or pauses. MakerDAO has progressively decentralized its governance, but historical upgrades have occasionally paused the protocol. Research governance structures and upgrade mechanisms before committing significant funds.

High-Yield Strategies for DeFi Lending

Experienced DeFi participants employ several strategies to maximize yields while managing risks.

Strategy 1: Stablecoin Yield Farming

The most straightforward approach—supply stablecoins like USDC or USDT to earn 4-8% APY with minimal volatility. This approximates traditional high-yield savings without the FDIC insurance.

Expected Returns: 4-8% APY

Risk Level: Low (stablecoin de-peg risk exists)

Best For: Conservative investors, emergency fund alternatives

Strategy 2: Leverage Loop

Advanced users supply collateral, borrow stablecoins, then resupply the borrowed stablecoins to compound yields. This creates leverage but amplifies both gains and liquidation risk.

Expected Returns: 8-15% APY (leveraged)

Risk Level: High (liquidation risk multiplied)

Best For: Experienced users with high risk tolerance

Strategy 3: Cross-Chain Yield Optimization

Different chains offer varying yields due to competition for liquidity. As of January 2025, Polygon and Avalanche often offer higher yields than Ethereum mainnet due to lower competition for deposits.

Process: Bridge assets to multiple chains, supply to lending pools, monitor rates

Expected Returns: 5-10% APY

Risk Level: Medium (bridge risk, smart contract risk across chains)

Strategy 4: Governance Token Incentives

Protocols often distribute additional rewards in governance tokens to attract liquidity. Aave, Compound, and Morpho have all run incentive programs.

Considerations: Token value is volatile—APY calculations including token rewards are estimates. Impermanent loss on token price can exceed earned rewards.

DeFi Lending vs Traditional Finance Savings

For US-based investors, comparing DeFi yields to traditional options reveals significant differences—but also important distinctions in protection and accessibility.

Traditional Savings Options

| Option | Typical APY | FDIC/NCUA Insured | Access Time |

|---|---|---|---|

| Traditional Savings | 0.01-0.05% | Yes (to $250K) | 1-3 days |

| High-Yield Savings | 4.0-4.5% | Yes | 1-3 days |

| Money Market | 3.5-4.2% | Yes | 1-3 days |

| Certificates of Deposit | 4.25-4.75% | Yes | Locked term |

Rates from FDIC-insured institutions, January 2025

DeFi Lending Comparison

| Factor | DeFi Lending | Traditional Savings |

|---|---|---|

| Yield | 3-12% APY | 0.01-4.75% APY |

| Insurance | None (unless using covered protocols) | FDIC up to $250K |

| Access | Immediate (withdraw to wallet) | 1-3 business days |

| Minimum | Often $0-$100 | $100-$500 |

| Tax Reporting | Manual (complex) | 1099 provided |

| KYC Requirements | None typically | Full identity verification |

When DeFi Makes Sense

DeFi lending works best for investors who:

- Already hold cryptocurrency and want yield on holdings

- Understand wallet security and are comfortable self-custody

- Want higher yields than traditional options provide

- Can tolerate potential loss of principal

- Are comfortable managing tax implications independently

When Traditional Makes Sense

Traditional savings remains appropriate for:

- Those uncomfortable with self-custody

- Investors needing FDIC protection

- Those requiring regulated institutional recourse

- Simplicity-preferring users unfamiliar with crypto

- Funds needed for near-term expenses

Frequently Asked Questions

Q: Is DeFi lending safe?

DeFi lending carries several risks including smart contract vulnerabilities, liquidation during price volatility, and potential loss of principal. Major protocols like Aave have strong security track records but are not immune to exploits. Never invest more than you can afford to lose, and consider starting with small amounts to understand the mechanics.

Q: How do taxes work on DeFi lending interest?

In the United States, DeFi lending interest is generally treated as ordinary income and must be reported. The IRS has not issued specific guidance for DeFi, but interest received from lending likely qualifies as taxable income. You receive a 1099 from some centralized platforms, but self-custody DeFi requires manual tracking. Consult a tax professional for personalized guidance.

Q: Can I lose money lending on DeFi?

Yes. While lending protocols are designed to return your principal plus interest, you can lose money through smart contract exploits, borrower liquidations that leave insufficient reserves, or stablecoin de-pegging (like the collapse of UST in May 2022). Your principal is not FDIC-insured.

Q: What’s the minimum amount to start DeFi lending?

Most DeFi lending platforms have no strict minimum, but transaction fees (gas) make small deposits impractical. On Ethereum mainnet, gas for a supply transaction typically costs $5-30, making deposits under $1,000 inefficient. Layer 2 networks like Arbitrum or Base reduce gas to under $0.50, enabling smaller starting amounts.

Q: How often is interest paid in DeFi lending?

Interest accrues continuously—calculated per block (approximately every 12 seconds on Ethereum). Your balance increases with each block, and you can withdraw accrued interest at any time without penalty. This compound interest effect accelerates returns compared to monthly or annual payments.

Q: What’s the difference between Aave, Compound, and MakerDAO?

Aave offers the largest liquidity and cross-chain deployment with variable rates. Compound focuses on simplicity with its V3 release, removing features for a streamlined experience. MakerDAO generates the DAI stablecoin through collateralized debt positions rather than functioning as a pure lending pool. All three are established protocols with strong security histories.

Conclusion and Action Steps

DeFi lending platforms offer a compelling alternative to traditional savings, with yields 5-20x higher than conventional banks. The space has matured significantly since the early 2020 days, with major protocols like Aave and Compound demonstrating multi-year track records and robust security practices.

IMMEDIATE ACTION STEPS:

| Timeframe | Action | Expected Outcome |

|---|---|---|

| Today (30 min) | Set up MetaMask wallet and verify seed phrase storage | Secure wallet ready for DeFi |

| This Week (1-2 hrs) | Research platforms, acquire $500-1000 in stablecoins via exchange | Assets ready to deploy |

| This Month (ongoing) | Supply assets to Aave V3 on Layer 2 (Arbitrum/Base), start with 50% of planned capital | Earn 4-6% APY on holdings |

CRITICAL INSIGHT:

The biggest mistake new DeFi lenders make is jumping straight to yield optimization strategies before understanding basic platform mechanics. Start with simple stablecoin supply on a Layer 2 network to minimize gas costs while learning. Only after comfortable with the process should you explore borrowing, leverage loops, or cross-chain strategies.

FINAL RECOMMENDATION:

For most readers, the optimal starting point is supplying USDC or DAI on Aave V3 deployed to Arbitrum or Base—these networks offer yields of 5-7% APY with transaction fees under $0.50. This combination minimizes complexity while maximizing net returns after accounting for gas costs.

TRANSPARENCY NOTE:

This article was written for educational purposes. We hold positions in AAVE and COMP as personal investments but received no compensation from any platform mentioned. DeFi protocols change frequently—verify current rates and contract addresses directly on official platforms before making transactions. Cryptocurrency investments carry substantial risk including potential total loss.

Article prepared January 25, 2025. DeFi yields and TVL figures are as of publication date and will fluctuate with market conditions.