Emergency Fund Calculator: How Much Do You Really Need?

Building an emergency fund is one of the most important financial steps you can take, yet most Americans are unprepared. According to the Federal Reserve’s Survey of Household Economics , only 44% of adults could cover a $1,000 emergency expense using savings. An emergency fund calculator helps you determine exactly how much you need based on your unique financial situation, not generic “three to six months” rules that don’t account for your specific circumstances.

This guide breaks down how emergency fund calculators work, the factors that influence your ideal savings target, and how to build your fund step by step.

What Is an Emergency Fund and Why It Matters

An emergency fund is money set aside specifically to cover unexpected financial shocks—job loss, medical emergencies, major car repairs, or home repairs that could otherwise derail your finances. Unlike other savings goals, this money must be readily accessible, typically in a high-yield savings account.

The purpose is simple: prevent you from borrowing money at high interest rates when life throws you a curveball. Whether it’s a $500 car breakdown or a $5,000 medical bill, having dedicated emergency savings means you won’t rack up credit card debt or dip into retirement accounts early.

Financial experts consistently emphasize the psychological benefit as well. Having three to six months of expenses saved reduces financial anxiety and provides peace of mind that you can handle whatever comes next.

How Emergency Fund Calculators Work

Emergency fund calculators take the guesswork out of determining your target savings amount. Rather than arbitrarily aiming for three or six months of expenses, these tools analyze your specific financial situation to produce a personalized recommendation.

The Basic Calculation Method

Most emergency fund calculators use this fundamental formula:

Monthly Expenses × Months of Coverage = Target Emergency Fund

However, the “monthly expenses” and “months of coverage” inputs vary significantly based on your personal circumstances, which is where calculators add value.

Factors Calculators Consider

A quality emergency fund calculator will ask about several key factors:

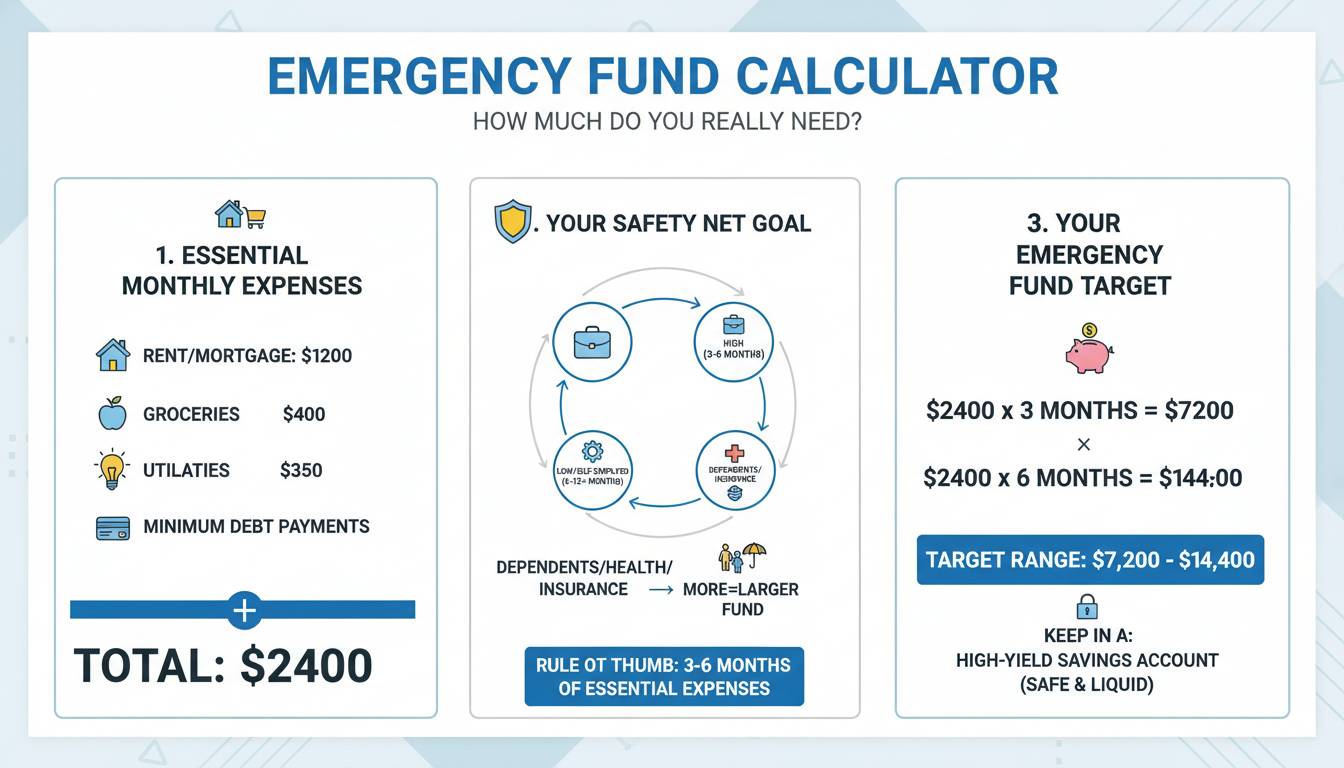

Fixed Monthly Expenses: Your rent or mortgage, car payment, insurance premiums, utility averages, subscription services, and minimum debt payments. These are non-negotiable costs you must cover regardless of your situation.

Variable Expenses: Groceries, gas, entertainment, and discretionary spending. These can be reduced in an emergency but still need to be accounted for.

Income Stability: Whether you’re salaried with a stable employer, self-employed with variable income, or work in an industry with cyclical demand affects your recommended coverage period.

Household Composition: Single-income versus dual-income households, number of dependents, and whether you have a spouse or partner who could cover expenses if you lost income.

Health Considerations: Chronic health conditions or ongoing medical needs may require larger reserves.

Dependents and Obligations: Number of children, elder care responsibilities, or other financial obligations affect your target amount.

Recommended Coverage: How Many Months Do You Need?

Financial experts generally recommend three to six months of expenses, but the right answer depends entirely on your situation. Here’s how different profiles map to different recommendations:

Coverage Recommendations by Profile

| Profile Type | Recommended Coverage | Rationale |

|---|---|---|

| Single income, no dependents | 3-6 months | Fewer obligations, easier to find new employment |

| Dual income, no dependents | 3 months each | Two income streams provide redundancy |

| Single income with dependents | 6-9 months | Higher risk if primary earner loses income |

| Self-employed or freelance | 6-12 months | Income volatility is higher |

| Commission-based income | 6-9 months | Income fluctuates significantly |

| Health concerns or chronic conditions | 6-12 months | Potential medical costs and job searching challenges |

| Single-income household with children | 9-12 months | Maximum security for vulnerable families |

Step-by-Step: Calculating Your Emergency Fund

Here’s how to calculate your emergency fund target manually, following the same logic as most calculators:

Step 1: Calculate Your Monthly Essential Expenses

List all expenses you must pay every month to maintain your basic standard of living:

| Category | Monthly Amount |

|---|---|

| Rent/Mortgage | $1,500 |

| Utilities (avg) | $200 |

| Car payment | $400 |

| Car insurance | $150 |

| Health insurance | $300 |

| Groceries | $500 |

| Minimum debt payments | $200 |

| Childcare (if applicable) | $600 |

| Essential subscriptions | $50 |

| Total Essential | $3,900 |

Step 2: Add Discretionary Buffer (Optional)

Some calculators include a discretionary spending buffer (typically 20-30% of essential expenses) to account for lifestyle maintenance. If you’d struggle to cut back completely in an emergency, add this buffer:

$3,900 × 0.25 = $975 additional

Total with buffer: $4,875

Step 3: Multiply by Your Recommended Months

Using the profile recommendations from earlier:

- Single, stable job, renter: 3 months × $3,900 = $11,700

- Single earner with family, homeowner: 9 months × $3,900 = $35,100

- Self-employed: 12 months × $4,875 = $58,500

Common Mistakes When Calculating Your Emergency Fund

Mistake #1: Including Non-Essential Expenses

Many people calculate based on their current spending, which includes dining out, entertainment, and luxury purchases. In an emergency, these expenses can be dramatically reduced. Calculate based on essential expenses only—you can always save more, but aiming too high can feel impossible.

Mistake #2: Using Gross Income Instead of Expenses

Your emergency fund should be based on expenses, not income. Even if you earn $5,000 monthly but spend only $3,000, your fund should cover the $3,000 in expenses. The extra income provides additional cushion naturally.

Mistake #3: Ignoring Your Job Security Assessment

A common recommendation is “three to six months for everyone,” but this ignores that some jobs are far more secure than others. Government employees with tenure have different needs than startup employees in volatile industries. Be honest about your actual job security.

Mistake #4: Not Accounting for Household Changes

Major life changes—marriage, having children, buying a home—significantly change your emergency fund needs. Recalculate after any significant household change.

Building Your Emergency Fund: A Practical Timeline

Now that you know your target number, how do you actually build it? Here’s a practical approach:

Month 1-3: Establish the Foundation

Goal: Save $1,000 as a starter emergency fund

This baseline covers most minor emergencies—small medical bills, minor car repairs, unexpected home fixes. It prevents minor issues from becoming major debt problems.

Strategy: Automate transfers of $50-100 per paycheck to a dedicated high-yield savings account. Reduce one discretionary expense (subscription services, dining out) and redirect those funds.

Month 4-6: Expand to One Month Coverage

Goal: Save one month of essential expenses

With one month saved, you can handle a temporary job loss or larger unexpected expense without going into debt.

Strategy: Increase automated transfers. Consider a side hustle for three to six months to accelerate progress.

Month 7-12: Reach Three Month Coverage

Goal: Reach three months of expenses (or your personalized target)

This level provides meaningful protection against job loss or major emergencies.

Strategy: Continue consistent contributions. Tax refunds, bonuses, and side income should go directly to emergency savings until you reach your target.

After Target: Maintain and Grow

Once you reach your target, shift focus to maintaining it. If you ever withdraw from your emergency fund, make rebuilding it a priority before other financial goals.

Where to Keep Your Emergency Fund

Your emergency fund needs to be accessible but not too accessible. Here are the best options:

High-Yield Savings Accounts

Currently offering 4.00-4.50% APY (as of early 2025), high-yield savings accounts provide both accessibility and interest earnings. Your money is FDIC-insured and can be transferred within one to three business days.

Money Market Accounts

Similar to high-yield savings but may come with limited check-writing privileges. Currently offering similar rates around 4.00-4.25% APY.

Certificates of Deposit (CDs)

Not recommended for emergency funds unless you use a “CD ladder” approach, since early withdrawal penalties defeat the purpose of accessibility.

What to Avoid

- Checking accounts (too easy to spend)

- Investment accounts (too volatile)

- Cash at home (no interest, security risk)

- Cryptocurrency (extreme volatility defeats the purpose)

When to Adjust Your Emergency Fund

Your target isn’t permanent. Adjust your emergency fund in these situations:

Before major purchases: Temporarily boost your fund before buying a home or car to ensure you don’t deplete reserves.

After income changes: A raise might mean you can save more; a demotion or reduced hours means you might need more months of coverage.

After household changes: Marriage, divorce, having children, or children leaving home all warrant recalculation.

After job changes: Moving to a new industry or company affects your income stability assessment.

Frequently Asked Questions

How much should I save in my emergency fund if I’m self-employed?

Self-employed individuals should aim for six to twelve months of expenses, with nine months being a common target. Self-employment income volatility means you need a larger buffer than traditional employees. Calculate based on your lowest-earning month historically, not your average.

Can I invest my emergency fund in the stock market?

Generally, no. The purpose of an emergency fund is immediate accessibility, and market volatility means your money might be worth less when you need it. Keep emergency funds in high-yield savings or money market accounts. The slightly lower returns are worth the security.

Should I pay off debt or build an emergency fund first?

Financial experts typically recommend building a starter $1,000-2,000 emergency fund before aggressively paying debt. This prevents new debt if an emergency occurs while you’re paying off old debt. After that baseline, you can split extra payments between debt and building your full emergency fund.

What qualifies as an emergency fund withdrawal?

Only true emergencies justify tapping your emergency fund: job loss, medical emergencies, essential home or car repairs needed for work or safety. Vacations, holiday shopping, or sales are not emergencies—they’re planned expenses that should come from regular budgeting.

How long does it take to build an emergency fund?

Building a full emergency fund typically takes one to three years, depending on your income, expenses, and how much you can realistically save monthly. The key is consistency. Starting with even $25-50 per month builds the habit and provides some protection while you work toward your full target.

What if I already have some savings—is that my emergency fund?

Any dedicated savings can count, but the key question is: Would you be comfortable depleting this money for an emergency, or is it already designated for something else (vacation, down payment, gifts)? Your emergency fund should be separate from goal-specific savings and only used for true emergencies.

Conclusion: Your Next Steps

An emergency fund is foundational to financial security. Using an emergency fund calculator—or calculating manually using the methods above—gives you a specific, achievable target instead of an abstract goal.

Your immediate action steps:

- Calculate your number today: Use the expense worksheet above to determine your target based on your profile.

- Open a high-yield savings account: Rates are favorable, and the accessibility ensures your money is there when needed.

- Automate your savings: Set up automatic transfers, even small ones, to build the habit.

- Aim for $1,000 first: A starter emergency fund prevents most emergencies from becoming debt problems.

- Reassess annually: Your needs change as your life changes.

The best time to start building your emergency fund was yesterday. The second-best time is today. Even starting with $25 per week puts you $1,300 closer to financial security by this time next year.