How to Start Passive Income: Proven Methods for Beginners

The desire for financial freedom has never been more prevalent. Recent surveys indicate that 67% of Americans have considered ways to earn money outside their primary job, and searches for “passive income” have increased by over 150% in the past five years. Yet the term “passive income” remains widely misunderstood—most people envision automated wealth with zero effort, when in reality, successful passive income streams require upfront work, strategic thinking, and ongoing maintenance. This guide cuts through the hype to deliver practical, proven methods that beginners can actually implement, regardless of their current financial situation or expertise level.

The methods outlined here represent the most accessible entry points for generating income that continues working for you long after the initial effort. We’ll explore everything from low-capital digital approaches to investment strategies, examining the realistic earning potential, time commitments, and risk factors for each. By the end, you’ll have a clear roadmap for choosing and implementing passive income streams that align with your goals, resources, and risk tolerance.

Understanding Passive Income: Beyond the Myth

True passive income refers to earnings derived from assets or ventures in which you are not actively participating on a day-to-day basis. However, this definition requires an important caveat: almost every passive income stream demands significant initial effort, substantial capital, or both. The “passive” aspect refers to the lack of ongoing labor, not the absence of initial work.

Financial experts distinguish between three primary income categories. Active income comes from trading time for money—your traditional job or freelance work. Portfolio income derives from investments like dividends, interest, and capital gains. Passive income, the focus of this guide, flows from business activities in which you have invested money or effort upfront but don’t actively manage daily.

The distinction matters because it shapes expectations. A rental property generates passive income only after you’ve purchased the property, navigated tenant relationships, and established management systems. A digital course produces revenue only after you’ve created the content, built an audience, and set up sales infrastructure. Understanding this distinction prevents the disappointment that comes from unrealistic expectations.

Research from the Bureau of Labor Statistics shows that self-employed individuals who diversified into passive streams experienced 34% less income volatility during economic downturns compared to those relying solely on active income. This financial resilience represents one of the most compelling reasons to pursue passive income strategies, even if the initial returns seem modest.

The Most Accessible Passive Income Methods for Beginners

Not all passive income methods require substantial capital or specialized expertise. Several approaches offer relatively low barriers to entry while providing genuine potential for sustainable earnings.

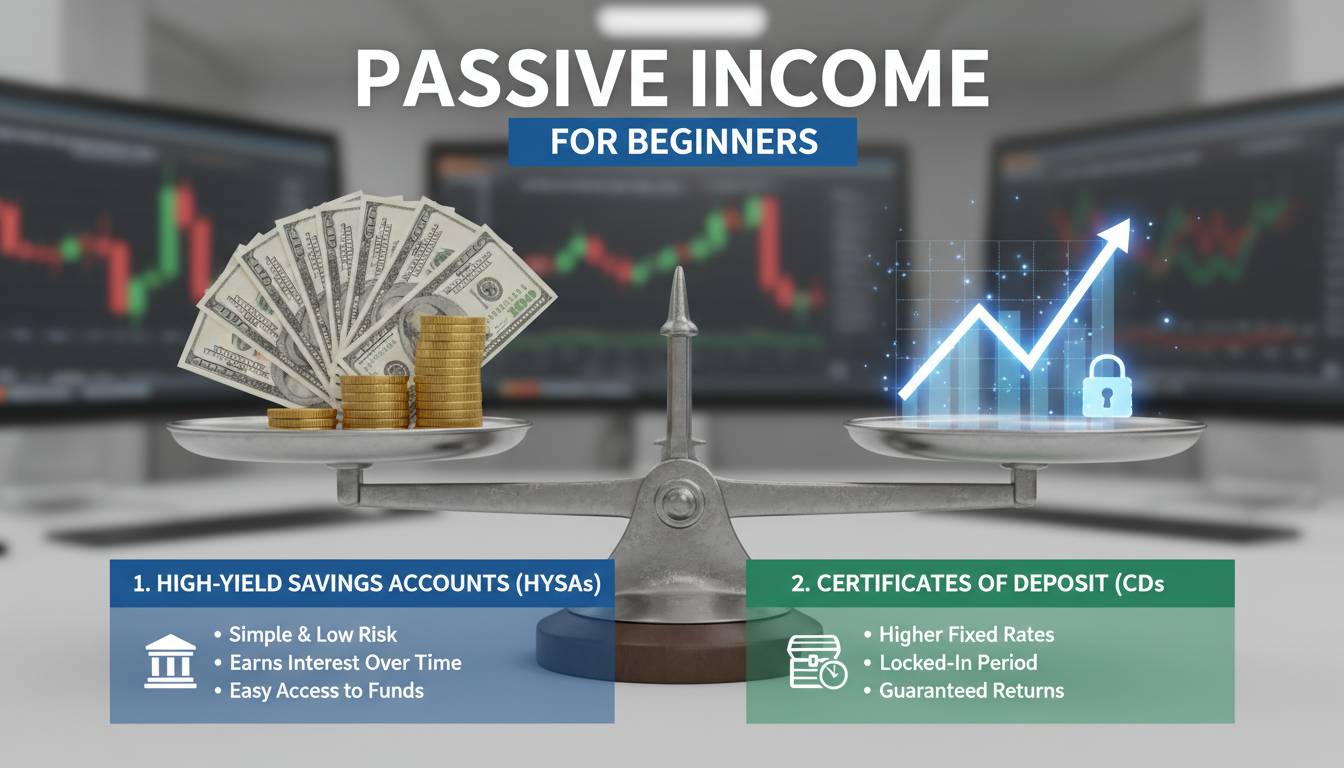

High-Yield Savings Accounts and Money Market Funds

For those just beginning their passive income journey, the simplest starting point involves placing capital in vehicles that generate interest. High-yield savings accounts currently offer annual percentage yields (APYs) around 4-5%, significantly better than traditional savings accounts averaging 0.5%. Money market funds, available through brokerage accounts, often yield 5% or higher with minimal risk to principal.

The math is straightforward: $50,000 deposited in a 4.5% high-yield account generates approximately $2,250 annually with zero effort. While this won’t replace a salary, it represents a foundation upon which to build. This method suits emergency funds or capital you want accessible while it works for you.

Dividend Investing

Dividend-paying stocks represent another accessible entry point. Companies like Johnson & Johnson, Procter & Gamble, and Realty Income have paid dividends consistently for decades, providing shareholders with quarterly income regardless of stock price movements. The average dividend yield for the S&P 500 hovers around 1.5-2%, though yield-focused funds can reach 3-4%.

Platforms like Fidelity, Schwab, and Vanguard make dividend investing accessible to anyone with a brokerage account and enough capital to purchase fractional shares. The key advantage: dividends require no additional work once you’ve selected your investments. Reinvesting dividends through a dividend reinvestment plan (DRIP) compounds your returns over time, accelerating wealth building.

Investment-Based Passive Income: Where to Start

Moving beyond basic savings, investment-based passive income offers higher return potential while requiring more knowledge and tolerance for risk.

Index Funds and ETFs

Index funds provide broad market exposure with minimal fees. A total stock market index fund like Vanguard’s VTSAX or iShares Core S&P Total US Stock Market ETF (ITOT) tracks the performance of thousands of companies, historically returning 7-10% annually over extended periods. These funds require no management decisions once purchased, making them the quintessential passive investment.

The investment approach works best when using dollar-cost averaging—investing a fixed amount monthly regardless of market conditions. This strategy removes emotional decision-making and historically outperforms attempts to time the market. For passive income purposes, dividend-focused index funds like Vanguard High Dividend Yield ETF (VYM) with its 2.6% yield provide regular income while maintaining growth potential.

Bonds and Bond Funds

For investors seeking more stability and predictable income, bonds offer fixed interest payments. Government bonds provide the lowest risk, while corporate bonds offer higher yields in exchange for accepting default risk. Bond funds like iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD) distribute monthly income from the underlying bonds in the portfolio.

The current interest rate environment has made bonds particularly attractive for income generation. Investment-grade corporate bonds now yield 5-6%, approaching equity-like returns with considerably less volatility. A $100,000 position in a 5% bond fund generates $5,000 annually—realistic passive income that requires only the initial capital allocation.

Digital Product Creation: Leveraging Your Knowledge

Perhaps no passive income method offers as much scalability as digital product creation. Once you’ve invested time in creating a product, it can sell indefinitely without additional production costs.

E-Books and Guides

Writing an e-book represents one of the lowest-cost ways to create a digital product. Platforms like Amazon Kindle Direct Publishing, Gumroad, and your own website enable distribution to global audiences. The key to success lies in choosing topics where you have genuine expertise and where an audience actively searches for solutions.

Successful e-book authors typically price their work between $2.99 and $9.99 for maximum sales volume. At a $5 average price with a 70% royalty rate, selling 200 copies monthly generates $700 in passive income. While this requires substantial upfront effort in writing and marketing, the ongoing income continues for years with minimal maintenance.

Online Courses

Online courses command higher price points than e-books, typically ranging from $49 to $497 depending on the topic depth and market demand. Platforms like Teachable, Kajabi, and Skillshare handle hosting, payment processing, and often provide marketing reach in exchange for revenue sharing.

The creation process requires significant upfront investment—most quality courses take 20-100 hours to develop. However, courses on practical topics like coding, digital marketing, personal finance, or professional skills can generate substantial ongoing revenue. Industry data suggests that successful course creators earn an average of $5,000-$15,000 annually from a single well-developed course, with some generating six figures.

Print-on-Demand

Print-on-demand services like Printful and Redbubble allow you to create custom designs for t-shirts, mugs, posters, and other products without holding inventory. When a customer purchases an item, the print-on-demand service prints, ships, and handles customer service while you receive the difference between the retail price and production cost.

This method requires design skills or willingness to hire designers, but the profit margins can be substantial. A t-shirt selling for $25 with $10 production cost generates $15 per sale. With effective designs and proper marketing, some creators generate $1,000-$5,000 monthly from print-on-demand businesses, making it one of the more profitable low-capital passive income methods.

Real Estate and Physical Assets: Traditional but Effective

Real estate has generated passive income for centuries, though it typically requires more capital than digital methods.

Real Estate Investment Trusts (REITs)

REITs offer real estate exposure without the complexities of property ownership. These publicly traded companies own income-producing properties—apartment buildings, office spaces, warehouses, retail centers, and data centers. By law, REITs must distribute 90% of taxable income as dividends, making them reliable income generators.

REITs like Prologis (industrial), Public Storage (self-storage), and Digital Realty (data centers) offer yields between 3-6% with professional management and daily liquidity. A $100,000 investment in a diversified REIT portfolio generates $3,000-$6,000 annually while allowing you to sell shares anytime. This combination of passive income, professional management, and liquidity makes REITs an attractive entry point to real estate.

Rental Property Ownership

Owning rental property remains one of the most tangible passive income methods, though it comes with responsibilities. Traditional rentals require active management—finding tenants, handling maintenance, dealing with vacancies. However, hiring a property manager shifts most day-to-day tasks while still providing ownership benefits.

The math works powerfully at scale. A $200,000 rental generating $2,000 monthly ($24,000 annually) provides a 12% cash-on-cash return before appreciation. After accounting for mortgage payments, property taxes, insurance, and management fees, net cash flow might reach $500-$1,000 monthly—real passive income once the initial work of acquiring and setting up the property is complete. Appreciation adds further wealth building potential over time.

Common Mistakes to Avoid on Your Passive Income Journey

Understanding what not to do proves as important as knowing which methods to pursue.

Mistake #1: Chasing Shiny Objects

The internet overflows with “passive income” promises—MLM schemes, cryptocurrency schemes, and get-rich-quick programs. Legitimate passive income requires genuine value creation, not recruitment or speculation. Before pursuing any opportunity, ask yourself: “Is this creating genuine value, or am I profiting from others’ participation?” The answer reveals whether the opportunity is sustainable.

Mistake #2: Starting Without an Emergency Fund

Building passive income while carrying high-interest debt (credit cards, personal loans) rarely makes mathematical sense. The guaranteed “return” from paying off 20% credit card debt exceeds the typical return from most passive investments. Financial advisors consistently recommend establishing 3-6 months of expenses in an emergency fund before pursuing passive income strategies that involve risk.

Mistake #3: Underestimating Initial Effort

Passive income becomes passive only after significant upfront work. Creating a digital course, acquiring rental property, or building an investment portfolio requires substantial initial effort. Those expecting immediate results often abandon strategies too soon. Committing to a 12-24 month timeline for seeing meaningful passive income prevents premature abandonment of viable strategies.

Mistake #4: Failing to Reinvest Returns

The most successful passive income builders reinvest their earnings to accelerate growth. That $500 monthly from a rental property becomes $1,000 when combined with another property. Dividend payments reinvested through DRIP dramatically increase compounding returns. Treating passive income as spending money rather than reinvesting capital limits long-term wealth building.

Building a Passive Income Stack: Combining Multiple Streams

The most resilient passive income strategy combines multiple streams rather than depending on a single source. This diversification provides stability—if one stream underperforms, others continue generating income.

A practical stacking approach might include:

- Foundation Layer: High-yield savings and bond funds providing stability and predictable income

- Growth Layer: Index funds and dividend stocks providing both income and capital appreciation

- Scalability Layer: Digital products offering high margins and unlimited scaling potential

- Inflation Hedge Layer: Real estate or REITs providing income that historically keeps pace with inflation

A beginner might start with a high-yield savings account while building knowledge, then add dividend investing, and eventually create a digital product or explore real estate. This graduated approach allows learning and adjustment while progressively building income streams.

Frequently Asked Questions

How much money do I need to start generating passive income?

The amount varies significantly by method. High-yield savings accounts require only $100-$500 to open. Dividend investing can begin with $100 using fractional shares. Digital product creation requires only time rather than capital. Rental properties typically require 20-30% down payment, making them the most capital-intensive option. Start with methods matching your current resources.

How long does it take to see returns from passive income?

Realistic timelines vary by method. High-yield savings generates immediate returns. Dividend investing typically shows meaningful results in 3-5 years. Digital products often take 6-18 months to generate significant sales. Rental properties can be cash-flow positive within the first year. Most methods require 2-5 years before generating substantial passive income.

Is passive income really “passive”?

Almost no passive income is completely effort-free. All methods require upfront work—research, capital deployment, content creation, or property setup. Some require ongoing attention—managing tenants, updating course content, or rebalancing investments. The key is that passive income doesn’t require trading hours directly for dollars once established.

What’s the safest passive income method?

High-yield savings accounts and US Treasury bonds represent the lowest-risk options, backed by government guarantees or high credit ratings. These provide modest but guaranteed returns. Higher returns always involve higher risk. A diversified approach combining several methods balances safety with growth potential.

Can I replace my full-time income with passive income?

It is possible but typically takes years of consistent effort. Most financial independence experts suggest building passive income equal to 50-100% of expenses before considering leaving traditional employment. This often requires $500,000-$1,000,000 in invested assets or highly successful digital businesses. Starting with the goal of supplementing employment income is more realistic initially.

Do I need special skills to create digital passive income?

Skills help but aren’t always required. Digital products succeed when they solve specific problems for defined audiences. You can hire designers, writers, or videographers if you have capital but lack skills. Alternatively, develop skills in areas like coding, graphic design, or writing to create products yourself. Many successful digital product creators started with minimal skills and learned as they built.

Conclusion

Building passive income represents one of the most powerful strategies for achieving financial independence and resilience. The methods explored in this guide—from accessible options like high-yield savings and dividend investing to more involved approaches like digital product creation and real estate—provide pathways regardless of your starting point.

The key to success lies in starting, even modestly. That first $500 invested in a high-yield account or the first hour spent developing a digital product begins the journey. As your knowledge grows and initial investments compound, you can expand into more sophisticated strategies.

Remember that genuine passive income requires upfront effort and often capital. The “passive” descriptor refers to the ongoing income generation, not the absence of initial work. By maintaining realistic expectations, avoiding get-rich-quick schemes, and consistently reinvesting returns, you can build passive income streams that provide genuine financial freedom over time.

Begin with one method that matches your current resources and comfort level. Master it before expanding. Financial independence doesn’t happen overnight, but the compound effect of consistent effort creates substantial wealth over years. Your passive income journey starts with the first step—and that step can be taken today.