DeFi Explained: The Ultimate Guide to Decentralized Finance

Decentralized Finance—commonly known as DeFi—has emerged as one of the most transformative developments in the financial technology landscape. In 2024, the total value locked in DeFi protocols surpassed $100 billion, representing a fundamental shift in how individuals and institutions access financial services. Unlike traditional banking, which relies on intermediaries like banks and brokerages, DeFi operates through blockchain technology, enabling peer-to-peer transactions that are transparent, permissionless, and available to anyone with an internet connection.

This comprehensive guide explores the mechanics, applications, risks, and future trajectory of decentralized finance, providing you with the knowledge needed to understand this rapidly evolving sector.

What is Decentralized Finance?

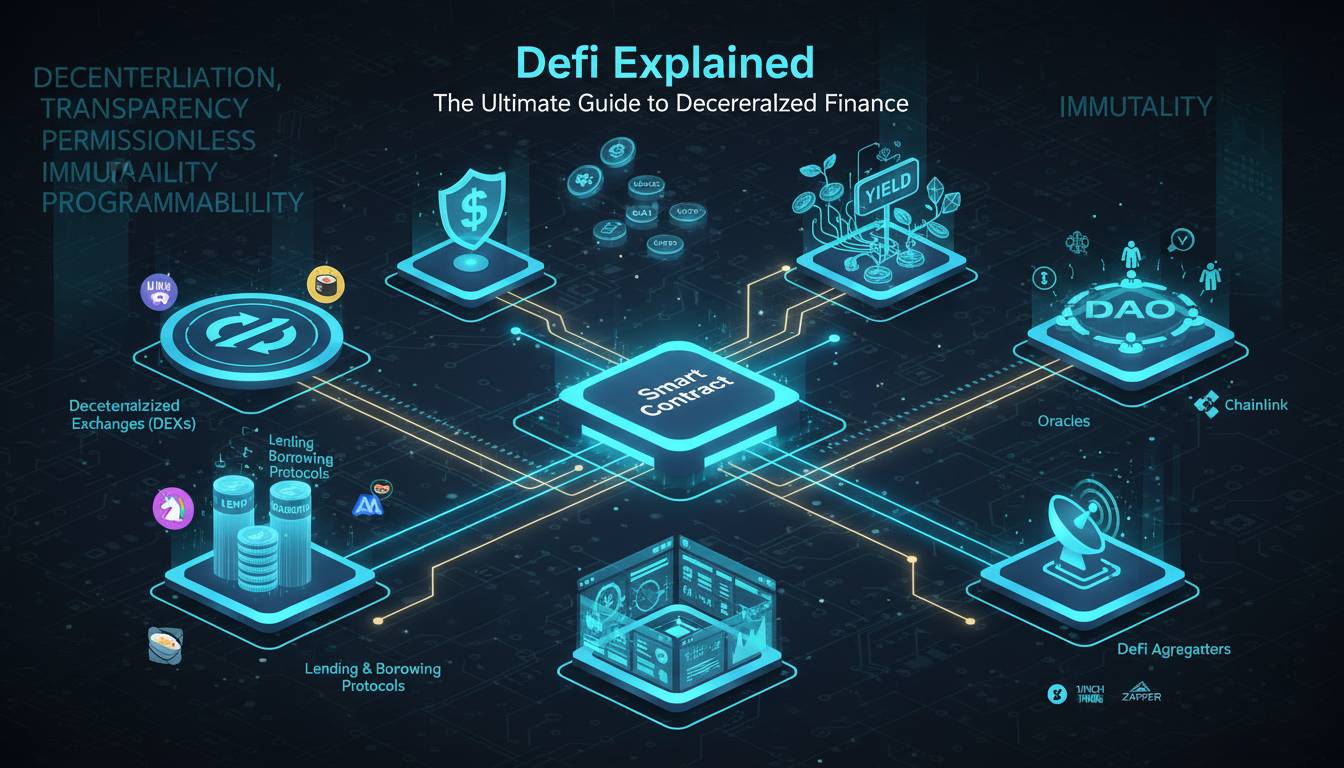

Decentralized Finance refers to a collection of financial applications built on blockchain networks—primarily Ethereum—that aim to recreate traditional financial instruments without centralized intermediaries. These protocols enable activities such as lending, borrowing, trading, and earning interest on assets, all through smart contracts that automatically execute when predetermined conditions are met.

The DeFi ecosystem emerged from the realization that traditional financial systems, while functional, create significant barriers: geographic restrictions, high fees, slow settlement times, and the need for extensive documentation and credit checks. DeFi addresses these pain points by removing the middleman and replacing human-controlled institutions with code.

Key Characteristics of DeFi:

- Permissionless Access: Anyone can participate regardless of location or background

- Transparency: All transactions and code are publicly viewable on the blockchain

- Interoperability: Protocols can be stacked and combined like financial Lego blocks

- Custodyless: Users retain control of their assets through personal wallets rather than trusting a third party

The concept gained mainstream attention starting in 2019-2020, when lending protocols like Compound and Aave began offering substantial yield farming incentives. According to data from DeFiLlama, the DeFi sector has grown from approximately $1 billion in total value locked in early 2020 to peaks exceeding $180 billion in late 2021 before settling into its current range.

How DeFi Works: The Building Blocks

Understanding DeFi requires grasping several interconnected technical and economic concepts that form its foundation.

Smart Contracts

At the core of DeFi are smart contracts—self-executing programs deployed on blockchain networks that automatically enforce the terms of an agreement. When you lend money through a DeFi protocol, the smart contract holds your funds and automatically distributes interest to your wallet based on predefined rules. There is no bank officer reviewing your application or processing your transaction manually.

Ethereum, launched in 2015, remains the dominant platform for DeFi applications, though competitors like Solana, Avalanche, and Binance Smart Chain have gained significant market share. The choice of blockchain affects transaction speeds, costs, and the available ecosystem of applications.

Liquidity Pools and Automated Market Makers

Traditional exchanges match buyers with sellers through order books. DeFi largely operates through liquidity pools—collections of tokens locked in smart contracts that facilitate trading. Users called liquidity providers deposit pairs of tokens into pools and earn fees from traders who swap between those tokens.

This system, pioneered by Uniswap in 2018, uses an Automated Market Maker (AMM) formula that prices assets algorithmically based on supply and demand within the pool. The mathematical formula ensures that trades can always be executed, though slippage—the difference between expected and actual trade prices—can occur during periods of low liquidity or high volatility.

Collateral and Overcollateralization

Because DeFi protocols cannot access traditional credit scores or legal systems for debt collection, they rely on overcollateralization. Borrowers must deposit crypto assets worth significantly more than the value of the loan they wish to take. If the value of the collateral falls below a certain threshold, the position is automatically liquidated to protect lenders.

This system, while seeming inefficient, enables secure lending without credit checks. Popular lending protocols like Aave and Compound allow users to collateralize assets like Ethereum, Wrapped Bitcoin, or stablecoins to borrow other assets or receive flash loans.

Key DeFi Use Cases and Applications

The DeFi ecosystem has developed numerous applications that mirror—and in some cases improve upon—traditional financial services.

Lending and Borrowing

DeFi lending platforms allow users to earn interest on their crypto holdings by supplying liquidity to borrowing pools. Interest rates are determined algorithmically based on supply and demand, often yielding returns significantly higher than traditional savings accounts. As of 2024, competitive yields on stablecoin deposits commonly range from 3% to 8% annually, compared to less than 0.5% for conventional savings accounts.

Borrowers can access instant loans without credit checks, using their crypto holdings as collateral. This capability enables several strategic use cases: leverage trading, avoiding taxable events by borrowing against assets rather than selling them, and accessing liquidity without leaving the crypto ecosystem.

Decentralized Exchanges

Decentralized exchanges (DEXs) like Uniswap, Curve, and SushiSwap enable token swaps directly from users’ wallets without transferring funds to a centralized custodian. This eliminates counterparty risk—the possibility that the exchange might be hacked, go bankrupt, or misuse user funds.

Trading volumes on decentralized exchanges have grown substantially, with 24-hour volumes regularly exceeding $10 billion across major platforms. The ability to trade without KYC (Know Your Customer) verification remains a significant privacy advantage, though it has also attracted regulatory scrutiny.

Yield Farming and Staking

Yield farming involves strategically moving assets across different DeFi protocols to maximize returns. Advanced practitioners may deposit tokens into a liquidity pool, receive governance tokens as rewards, stake those rewards for additional yield, and then use the staked tokens as collateral for further borrowing.

Staking, while related, typically refers to locking up cryptocurrency to support network operations—particularly for proof-of-stake blockchains like Ethereum. Stakers receive rewards for helping secure the network and validating transactions. Ethereum’s transition to proof-of-stake in 2022 made staking accessible to regular users, with current annual yields of approximately 3-5% for ETH stakers.

Popular DeFi Protocols and Platforms

The DeFi landscape features hundreds of protocols, but several have established themselves as foundational infrastructure.

| Protocol | Category | TVL (2024) | Primary Function |

|---|---|---|---|

| Lido | Liquid Staking | ~$30B | ETH staking with liquid token |

| Aave | Lending | ~$15B | Collateralized borrowing |

| Uniswap | DEX | ~$5B | Token swapping via AMM |

| Curve | DEX | ~$3B | Stablecoin and correlated asset trading |

| MakerDAO | Lending | ~$5B | DAI stablecoin generation |

Lido Finance has become particularly significant in the Ethereum ecosystem, allowing users to stake any amount of ETH and receive stETH—a liquid token that can be used in other DeFi protocols while still earning staking rewards. This innovation solved a key problem with native Ethereum staking, which requires exactly 32 ETH and locks funds indefinitely.

Aave pioneered flash loans—a unique DeFi innovation allowing users to borrow substantial amounts without collateral, provided the loan is repaid within a single blockchain transaction. While flash loans have been used for arbitrage and liquidity provision, they also represent a powerful financial primitive impossible in traditional finance.

Risks and Challenges in DeFi

Despite its innovation, DeFi carries substantial risks that participants must understand before engaging.

Smart Contract Vulnerabilities

DeFi protocols are only as secure as their underlying code. Bugs or exploits in smart contracts can lead to catastrophic losses. According to blockchain security firm CertiK, DeFi hacks resulted in approximately $2.5 billion in losses during 2023 alone. Notable incidents include the Ronin Bridge exploit ($625 million in 2022) and the Euler Finance hack ($197 million, most of which was later recovered).

The immutable nature of blockchain means that once funds are stolen, recovery is extremely difficult. While code audits and bug bounty programs help identify vulnerabilities, they cannot guarantee security.

Impermanent Loss

Liquidity providers on AMM-based DEXs face a phenomenon called impermanent loss—a reduction in the value of their holdings compared to simply holding the assets. When the price ratio between two tokens in a pool changes significantly, liquidity providers may find they would have been better off simply holding the tokens rather than providing liquidity.

This risk is particularly pronounced for volatile asset pairs and represents one of the most misunderstood aspects of yield farming. Many novice liquidity providers have suffered substantial losses without understanding the mechanism.

Regulatory Uncertainty

The regulatory landscape for DeFi remains unclear and varies significantly by jurisdiction. While DeFi protocols are technically permissionless, governments increasingly require compliance with Know Your Customer and Anti-Money Laundering regulations. The U.S. Securities and Exchange Commission has signaled that some DeFi tokens may constitute securities, potentially imposing significant compliance burdens on developers and users.

The Future of Decentralized Finance

The trajectory of DeFi points toward greater institutional adoption, improved infrastructure, and potential regulatory frameworks.

Institutional players have begun entering the space, with major financial firms exploring tokenized real-world assets, on-chain treasuries, and regulated lending platforms. BlackRock’s tokenized fund initiative represents a significant vote of confidence in blockchain-based financial infrastructure.

Layer 2 scaling solutions—including Optimism, Arbitrum, and Base—have dramatically reduced transaction costs and increased throughput, making DeFi more accessible for everyday users. These improvements address historical criticisms about blockchain scalability while maintaining security guarantees.

The integration of real-world assets onto blockchain networks represents perhaps the most significant growth vector. Tokenized U.S. Treasuries, real estate, and private credit have the potential to bring trillions of dollars of traditional assets on-chain, dramatically expanding the DeFi ecosystem’s scale and utility.

Frequently Asked Questions

Is DeFi safe to use?

DeFi carries significant risks including smart contract vulnerabilities, smart contract risk, and total loss of funds. Users should only invest amounts they can afford to lose, use hardware wallets for large holdings, and thoroughly research protocols before committing funds. Even well-audited protocols have been exploited, so no DeFi investment is entirely risk-free.

How do I start using DeFi?

To begin using DeFi, you’ll need a cryptocurrency wallet like MetaMask, some cryptocurrency (typically Ethereum or tokens on EVM-compatible chains), and gas fees for transactions. Start by connecting to a reputable decentralized exchange like Uniswap to swap tokens, then explore lending protocols or liquidity pools that match your risk tolerance.

What is the difference between CeFi and DeFi?

Centralized Finance (CeFi) involves traditional financial institutions that hold your assets and facilitate transactions—similar to conventional banks. DeFi eliminates intermediaries, giving users direct control over their funds through non-custodial wallets and automated smart contracts. CeFi offers customer support and regulatory protection; DeFi offers transparency and potential higher yields but requires users to manage their own security.

Can I lose money in DeFi?

Yes, you can lose all your money in DeFi through several mechanisms: smart contract exploits that drain protocol funds, impermanent loss from liquidity provision, liquidation of collateral during price volatility, and complete loss of access if you lose your wallet seed phrase. Unlike traditional bank accounts, there are no government guarantees or recovery mechanisms for lost or stolen DeFi funds.

What are gas fees in DeFi?

Gas fees are transaction costs paid to blockchain validators for processing operations. On Ethereum mainnet, gas fees can fluctuate significantly based on network congestion—sometimes costing $10-50 for complex DeFi transactions during peak periods. Layer 2 solutions and alternative blockchains offer much lower fees, making them preferable for smaller transactions.

Is DeFi legal?

DeFi’s legal status varies by jurisdiction and continues to evolve. Some activities may require licensing or compliance with securities regulations. Users should consult legal professionals familiar with cryptocurrency regulations in their country. While the technology itself is legal in most jurisdictions, specific use cases and token distributions may trigger regulatory requirements.